policies are not just investments for securing the future but can also serve as valuable assets during times of financial need. One of the lesser-known benefits of owning an LIC policy is the option to avail of a loan against it. This facility allows policyholders to access funds quickly without liquidating their policy. If you’re considering this option, here’s a comprehensive guide on how to get a loan against LIC policy in 2024 in India.

Loan against LIC Policy in 2024

A life insurance policy aims to give financial protection to the survivors of the policyholder in the event of the death of the insured. There are different kinds of policies that give this benefit- Term insurance plans, endowment, money back, whole life, or Unit Linked Insurance Plans.

Term insurance policies pay the sum insured only in the event of death. On the other hand, endowment policies/money back policies or Whole Life policies make payments to the insured on surviving a certain number of years or on maturity.

Many of the policies offered by the Life Insurance Corporation of India allow policyholders to raise requests for loans against the sum assured. This special feature helps LIC customers to take care of their liquidity needs for emergencies. To get a loan from LIC, policyholders are required to fulfill certain criteria and follow a standard procedure set forth by the company.

Table of Contents

Understanding Loan Against LIC Policy in 2024:

Before delving into the process, it’s essential to understand the concept of a loan against an LIC policy. Essentially, policyholders can leverage the surrender value of their policy to obtain a loan from LIC. The surrender value is the amount payable to the policyholder if the policy is terminated prematurely. This loan is typically offered at a lower interest rate compared to personal loans or credit cards, making it an attractive option for those in need of funds.

Policyholders have the option to access loans against their LIC coverage once the policy accumulates a surrender value. Typically, life insurance policies accrue a surrender value after the payment of two to three complete years’ premiums. This surrender value represents the amount payable to the policyholder if they decide to terminate their policies prematurely, before the policy term concludes.

Presently, policyholders holding such policies have the opportunity to obtain a loan from LIC, typically up to a certain percentage of the surrender value amassed. For the majority of active policies, the maximum loan amount that can be accessed is up to 90% of the surrender value. However, for paid-up policies, this limit is slightly reduced to up to 80% of the surrender value.

Policyholders are required to repay the loan amount along with accrued interest. LIC offers the flexibility for policyholders to continue paying interest on a half-yearly basis while deducting the loan principal amount from the claim benefit payout.

1. The rate of interest is declared by LIC every year and is further dependent on the policy type.

2. Interest rates on policy loans at LIC usually start from around 9%.

3. The interest on the loan is payable half-yearly.

4. LIC is liable to recover the outstanding amount and the interest payable from the claim proceeds at the maturity of the policy or on the death of the policyholder.

5. Loans can only be availed once the life insurance policy acquired a surrender value. Not all policies offer this benefit. Such provisions are detailed in the policy brochures of those that offer a loan facility.

6. LIC caps the minimum tenure during which a loan can be availed at is 6 months from the date of its issuance.

Eligibility Criteria:

To be eligible for a loan against your LIC policy, certain criteria must be met:

Policy Type

Not all LIC policies are eligible for a loan. Generally, traditional endowment policies, money-back policies, and whole life policies are eligible, while term insurance plans do not offer this option.

Policy Term

Most policies require a minimum number of years to have passed since the policy was purchased before you can avail of a loan. This period varies depending on the policy terms.

Surrender Value

The loan amount is typically a percentage of the surrender value of the policy. Therefore, policies with higher surrender values offer larger loan amounts.

Premium Payment

Policyholders must have paid premiums regularly for a certain number of years to qualify for a loan. Policies in default or lapse status may not be eligible.

Addition to the above mentioned points, there are few more like the policyholder should be a citizen of India, the policyholder should be a minimum of 18 years of age or above, the policy should have acquired surrender value.

Steps to Obtain a Loan Against LIC Policy in 2024:

Policy holders can obtain Loan against LIC Policy in 2024 by Two methods, i.e. they can either apply Online through LIC Official Website or they can choose the Offline Method by visiting any nearest LIC Branch.

Check Policy Eligibility

Verify whether your LIC policy is eligible for a loan and ensure that it has acquired a surrender value.

Calculate Loan Amount

Determine the maximum loan amount available against your policy. This information can usually be obtained from your policy documents or by contacting LIC.

Contact LIC Branch

Visit your nearest LIC branch or contact their customer service to inquire about the loan process. They will provide you with the necessary forms and documents required for the application.

Fill Out Application Form

Complete the loan application form provided by LIC. Ensure all information provided is accurate and up-to-date.

Submission of Documents

Along with the application form, you will need to submit supporting documents such as your policy document, identity proof, address proof, and bank account details.

Loan Processing

Once the application and documents are submitted, LIC will process your loan request. This typically takes a few days, during which LIC will verify the details provided.

Disbursement of Loan

Upon approval, the loan amount will be disbursed directly to your bank account. You will also receive a loan sanction letter outlining the terms and conditions of the loan.

If the policy holder opts for going through the online channel, he/she should have a online account in the LIC Portal.

Customer Portal

There he/she has to hover to “Online Services”, and then to “Online Loan”.

Then he/she has to login into their account by their User ID, Password and DOB.

Login Details

Then he/she has to select the policy against which Loan is required.

Then he/she can choose the loan amount, EMI payment options, interest payable, and the tenure of the loan.

Then he/she has to submit the relevant documents and then they can proceed to make a request.

Repayment of Loan

Loan repayment terms vary depending on the policy and the loan amount.

Typically, LIC allows policyholders to repay the loan in installments or in a lump sum.

Pay interest and the principal in loan EMIs. Interest is charged on the outstanding loan amount, which is deducted from the policy’s surrender value. Pay only the interest regularly and pay principal in due course.

Failure to repay the loan may result in a reduction of the policy benefits or even policy lapse.

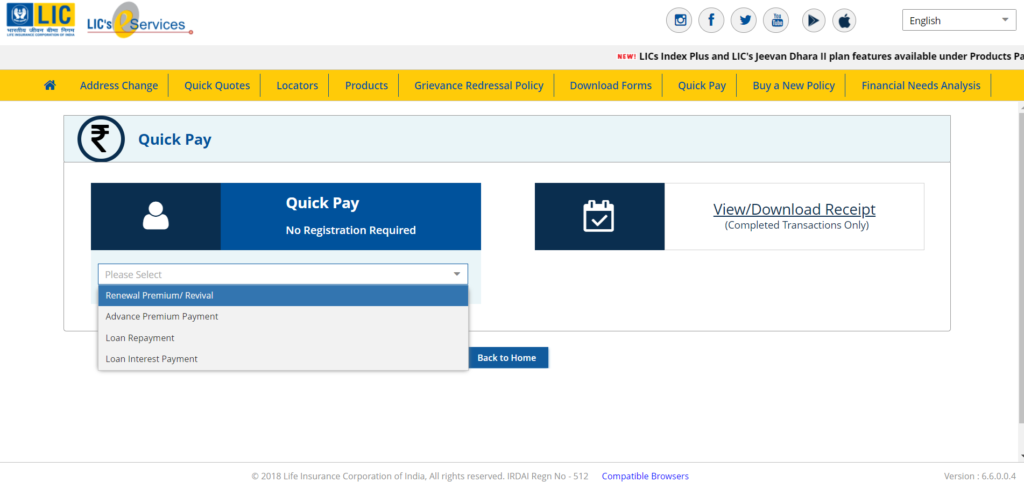

If he/she wants to repay using Online method, then this facility is also available. Click on the ‘Online Loan’ tab under ‘Online Services’, then a new page would be displayed ‘Online Policy Loan Options’ page. Under the Loan Repayment/ Loan Interest Payment section, you will see two options, viz. Pay Direct and Pay Through Customer Portal.

Repayment Option

Pay Direct

From the drop-down menu, select either Loan Repayment or Loan Interest Payment. Fill in the requested details in the form fields for ‘Customer Validation’ and ‘Loan Particulars’ and then make Payment.

Pay Through Customer Portal

He/she can Sign in with their User ID and Password. Then they can choose Loan Repayment or Loan Interest Payment and make Payment.

Conclusion

Availing a loan against your LIC policy can provide a convenient and cost-effective way to access funds during times of financial need. However, it’s essential to understand the terms and conditions associated with the loan and ensure timely repayment to avoid adverse consequences on your policy. By following the steps outlined in this guide and maintaining regular communication with LIC, you can make the most of this valuable feature of your LIC policy.